Cobblestone Financial

Structured Financial Solutions

Empowering you to achieve your financial and lifestyle goals

Over 30 Years Experience in Finance

How We Are Different

As your Mortgage Broker, it's our job to get to know you as a client. It is understanding your strengths and weaknesses. Learning what your goals are, now and in the future. It's about listening, I mean really listening, and then presenting a specific plan to help you achieve your goals.

What is important to you? What are your hopes and dreams? What does your retirement look like?

All of these questions will help design the correct facility that will work for you, leveraging on your strengths and putting strategies in place to ensure you reach your goals no matter what. This is not a set-and-forget process. This is an ongoing service.

Clients are for life.

Our Commitment to Service

We are committed to assisting you in finding the right finance option based on your information. We have the essential qualifications, experience and competency required under the relevant legislation to give you the professional service needed in assessing your financial needs.

You can be confident that we will deal with you fairly and ethically and take the time to listen to your requirements and objectives. Once we have established your goals, we will investigate and assess a range of options from our extensive lender panel. Ultimately, our primary aim is to provide you with a solution that explicitly matches your requirements. We will always act in your best interests.

We are National!

We offer services across Australia.

Frequently Asked Questions

Your Title Goes Here

Your content goes here. Edit or remove this text inline or in the module Content settings. You can also style every aspect of this content in the module Design settings and even apply custom CSS to this text in the module Advanced settings.

How much deposit do I need?

There are a few factors to this question...

In order to understand how much deposit you will need, you also need to understand 3 main components.

- Loan to Value Ratio (LVR)

- Lenders Mortgage Insurance (LMI)

- Stamp duty

Loan to Value Ratio or LVR

LVR is the amount borrowed divided by the property valuation.

For example, if your property is worth $500,000 and you borrow $450,000, you are borrowing 90% of the value of the property.

450 000 / 500,000 = 90%

This loan would be a 90% LVR

In this case, you would need a 10% deposit plus costs.

LMI or Lenders Mortgage Insurance

As a general rule of thumb, if you have less than 20% deposit, you will have to pay Lender Mortgage Insurance. LMI is an insurance policy that covers the lender, not the borrower, in the instance that you can’t make your repayments and the property is sold at a loss. Most of the time, LMI can be added to your loan in some instances. The higher the LVR, the more the Lenders Mortgage Insurance costs. For example, if you have an LVR of 85%, your LMI would be less than someone borrowing 95%. The higher the loan amount, the higher the LMI is again. Another example if you borrow 85% of 300K your LMI would be less than someone borrowing 85% of 600K.

Most people don’t save up 20% and usually want to get into a property with around 5-10% deposit, In this case, the borrower wouldn’t pay the LMI upfront but simply add it onto the loan. LMI is not always the enemy though. Firstly it allows you to get into a home sooner and start paying off your mortgage instead of renting. Secondly, if you are an investor, it allows you to purchase additional properties with a reduced deposit, getting you into the investor market sooner, accumulating more property, and staring your journey towards wealth creation.

Most states have a government intuitive for lower-income earners to get into a property with as little as a 2% deposit. These loans are exempt from LMI, however, it comes as a price by way of a higher interest rate. Generally 1 ½ - 2 percent above the market rate.

Stamp duty

This is the government tax you pay when you buy a house. You must pay this tax every time you buy a house. If you are a First Home Buyer, you may be eligible for Stamp Duty exemption or concession, which can save you thousands of dollars. If you are not eligible for Stamp exemptions, this is another substantial cost you will need to factor into your calculations.

Examples

Let's look at a few different scenarios on a purchase price of $400,000 assuming there is no Stamp duty payable as it is a First Home Buyer.

I have 2% deposit.

2% x $400,000 = $8,000

If you are a single parent or guardian, you may be eligible for a Family Home Guarantee with just 2% deposit and avoid LMI altogether.

There are some lenders that offer 98% LVR for those who are not eligible for a scheme loan, however, your interest rates are higher than current market rates.

Other lenders offer 98% loans where you might be charged a risk fee instead. Sometimes getting out of these loans can be quite difficult as you need to pay down your loan in order to get out of the higher rate bracket.

I have a 5% deposit.

5% x $400,000 = $20,000

Great! You are eligible for a 95% Lend, which opens up a lot more options.

If you are a First Home Buyer, you may be eligible for a First Home Buyers Guarantee with just 5% deposit and avoid LMI altogether.

If you are not a first home buyer, you still have options. Some lenders will let you capitalise the LMI on top of your loan so long as the combined loan and LMI does not exceed 98% LVR. You may still have to pay a higher interest rate until you can bring your loan down below 90%.

I have a 10% deposit.

10% of $400,000 = $40,000

Even better, at 90% LVR you can pretty much use most lenders. Your rate is most likely to be at market price or just above and you could capitalise the LMI if you wanted to.

I have a 20% deposit

20% of $400,000 = $80,000

You can use any lender you like, so long as you fit within their guidelines. At this LVR you will probably get a very competitive interest rate and you will not have to pay Lenders Mortgage Insurance at all.

As you can see there are many factors to consider. This is really just the basics as there are many more considerations in choosing the right lender that may include the postcode you are buying in, the type and size of the property, the ages of the borrowers, the type of employment of the borrowers and the savings history. Using a broker who has experience in these loans will save you a lot of time and also a lot of money. It’s important to find an expert to help you navigate such a huge decision.

What are my purchase costs going to be?

Things to consider when buying your first home:

- The Deposit

- Loan to Value Ratio

- Lenders Mortgage Insurance

- Stamp Duty Concessions

- Fees

- The Lender

The Deposit

The deposit for your first home can come from a number of sources: A gift or inheritance, the sale of an asset, genuine savings, or the First home owners grant. Different lenders have different policies regarding the source of your deposit. Generally, the bigger the deposit, the more flexible they are. If you only have a small deposit, most lenders want it to be genuine savings shown over 3 months. Some lenders may also consider the rent you have paid over 6 months in lieu of lump sum payments. Your deposit will determine a number of things: The LVR of your loan and also the LMI payable.

Loan to Value Ratio

Your deposit determines the LVR. If you have a 5% deposit plus costs, your LVR will be 95%. In other words, you are borrowing 95% of the value of your home and putting a 5% deposit towards your purchase. If you have a 10% deposit plus costs, the LVR will be 90%. In other words, you are borrowing 90% of the value of your home and putting a 10% deposit towards the purchase and so on. The lower the LVR, the lower the risk in the eyes of the Lender. This higher the LVR, the higher the risk.

Lenders Mortgage Insurance (LMI)

Any deposit less than 20% of the value of the property will incur Lenders Mortgage Insurance (LMI). LMI does not provide protection for you as the borrower but is a type of insurance that covers the bank or lender in the event that a home buyer was unable to repay their home loan and the property was sold by the bank at a loss. The cost of LMI can range from $1,000 to $20,000 or more depending on the size of your deposit and how much you need to borrow. The LMI amount can be paid upfront or added to your home loan. Most people don’t save up 20% and usually want to get into a property with around 5-10% deposit. In this case, the borrower wouldn’t pay the LMI upfront but simply add the insurance cost to the loan amount. This is called capitalizing the LMI. For example, if they had a 50K deposit for a 500K purchase. The loan is 90% so LMI is applicable. The LMI premium is $7,920 which can be added to the loan. The final loan amount is $450,000 + $7,920 = $457,920 (with the LMI capitalized), not including fees for simplification. There are grants and policies available to help borrowers avoid LMI. The First Home Buyers Guarantee, The Family Home Guarantee and various profession-specific policies which waive the LMI for eligible borrowers. See our Grants and Schemes section or contact us to see if your profession is eligible for an LMI waiver. LMI is not always the enemy - Why? Well, firstly it allows you to get into a home sooner and start paying off your mortgage instead of renting. Secondly, if you are an investor with a 20% deposit, instead of buying 1 property at 80% LVR, you could purchase 2 properties with a 10% deposit on each at 90% LVR. This allows you to accumulate more property, and start your journey towards true wealth creation.

Stamp Duty

Stamp duty or Land transfer duty is the tax you pay to the Government when you purchase a block of land or an established property. Every time this property is sold, the purchaser will need to pay Stamp Duty to the Government. If you are a First Home Buyer, you may be eligible for a stamp duty concession or exemption – First Home Owners Rate of Duty. To be eligible for the FHOR of duty, there are thresholds to be aware of. Find links to information about each state's First Home Owners Grant.

Fees

There are a number of different fees to be aware of when purchasing a property. Firstly, when you find something you like, you will want to conduct a building inspection before making an offer as well as a pest inspection to check for termites etc. These are both out-of-pocket expenses that must be paid upfront by the buyer before you sign the contract. Secondly, once you have had your offer accepted, you may have to pay for a valuation. Many of the main lenders offer free valuations, but if you are going with someone a little more boutique, you will likely need to pay prior to submitting your loan. As part of your finance application, there may be other fees payable to the lender such as application fees and settlement fees. Sometimes these can be waived so speak to your broker about this before submission. There are also government fees which include Land Transfer fees and Mortgage Registration fees, then there is stamp duty if you are not a first home buyer or if your purchase is over the threshold amounts set by the government in your state. Finally, you will need a good settlement agent to facilitate the settlement. These professionals charges fees. They will act on your behalf and ensure the settlement is executed as planned. They are an important part of the process so make sure you find a good one. All of these fees need to be considered when determining the fund you need to complete the purchase. These must be made available on settlement on top of your deposit. If there is any shortfall come settlement time, the sale could fall through. As your broker, we will give you an estimate upfront, but it will be your settlement agent's job to ensure there are enough funds to complete on the day. Please see the fees outlined below: Funds to Complete (approximately)

- Building inspection: $300

- Pest Inspection: $300

- Valuation: $300

- Application fee: $250

- Settlement fee: $600

- Land transfer: $250

- Mortgage registration: $180

- Conveyancer / Settlement agent: $800 to $1,800 depending on complexity

- Stamp duty: $1000 to $20,000 plus depending on loan amount.

Note: Stamp may be applicable if you are not a first home buyer or the property value is over the threshold in your state. Calculate your stamp duty below, or contact us and we can give you a full cost analysis. Calculate Stamp duty:

- ACT Calculator

- NSW Calculator

- VIC Calculator

- WA Calculator

- NT Calculator

- QLD Calculator

- SA Calculator

- TAS Calculator

The Lender

Finally, there are many things to consider when choosing a lender: Some lenders offer to capitalize your LMI, and some do not. Some lenders capitalize LMI & charge you a higher rate as the risk is higher. Other lenders charge you a higher rate if your Loan to Value Ratio is high ie above 90% LVR. Some lenders have great post-settlement variation processes, allowing you to transition to a lower rate once you have paid off some of your loan, whilst others, do not. With so many considerations, it can be overwhelming to buy your first home. This is why it is best to talk to your Mortgage Adviser, as they can help you work out which is the best option for you.

How do I go about refinancing?

Refinancing made easy

The thought of refinancing can be daunting but switching for a better interest rate or specific feature, can actually save you thousands of dollars each year. It really only takes about 1 to 2 hours of your time to complete all of the necessary tasks & we do try to make it as simple as possible for you.

Here are some ways we have managed to streamline the process for you.

Video or Phone Meetings

Getting to a meeting can be difficult, especially when you have kids, work or a FIFO partner. We offer our clients several options to work around your busy schedules. You can come to our office if you prefer, or you can choose to book in a video or phone meeting at a time that suits you. Our simple online booking system allows you to choose the type of meeting you want, at a time and day of your choosing.

Client Portal

After your initial meeting, you will be invited to our Client Portal. Our Client Portal is one of the most advanced on the market today. Not only does it allow easy communication between yourselves and your broker, but you can also see exactly where your application is up to. You can use the portal to upload documentation, download paperwork and leave notes for your broker. You are never left wondering what stage your application is at.

Paperwork

Forget about spending hours completing paperwork. All of our forms are pre-filled for you based on the information you have given us and all that will be required is a signature.

E-Signatures

Wherever possible, we use electronic signatures. You will receive an email to say the document is ready to sign. You can sign the document on your computer or your phone instantly anywhere, anytime. All documents are stored in a secure cloud storage service with advanced encryption and two-factor authentication.

Bankstatements.com

No need to go into a branch, we use a secure service that allows you to log in to your online banking and have your statements retrieved and automatically sent to us. It is provided by an Australian company and it takes less than 30 seconds.BankStatements is independently designed and vetted by world-class security experts to ensure the highest levels of data protection and security.

On the Spot Credit Score Reporting

Sometimes you may have concerns about your eligibility to apply for a loan. This may be due to loss of employment in the past, getting into too much debt or extenuating circumstances such as a divorce or bankruptcy. We can do on the spot credit reports so that you know exactly where you stand right from the start. We will also work with you to turn your score around as quickly as possible to ensure you can present the best possible application.

Third-Party Authorities

We understand that obtaining tax returns if you are self-employed can be tedious. We offer our clients a simple solution by using 3rd party authorities to liaise directly with your accountant to collate the documentation that we need for your application.

Internet Banking

The final step in the process can also be the most overwhelming. To take the stress out of refinancing, we offer a post-settlement meeting to assist with setting up your Internet banking once the settlement is complete and redirecting your direct debits and automatic payments.

Should I be paying interest only, or principle and interest?

Firstly what is the difference between the two?

Principle and Interest Repayments

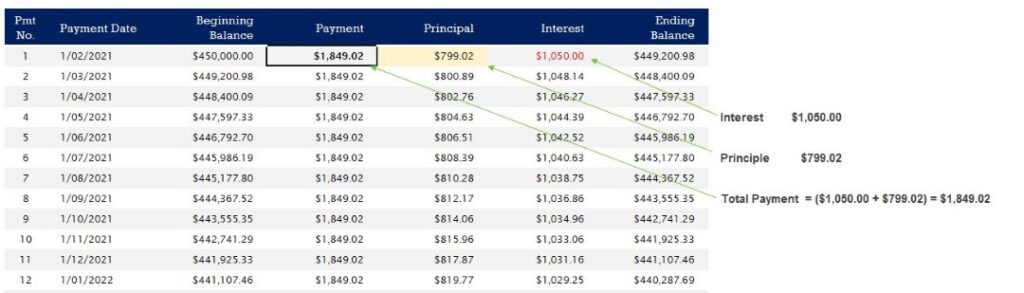

Principle and Interest repayments mean that your monthly repayment is made up of 2 components, the interest, and the principle. Or P&I. The interest is the part that goes to the lender at the agreed interest rate, and the principle is the part that goes towards paying down your loan amount. At the start of your loan, your interest makes up the majority of the repayment with a small amount making up the principle. It may feel like your loan is barely even moving at all when you first start making repayments. Over time, as your loan progresses, the interest payment gets smaller and the principle payment increases, even though your loan repayment stays the same each month. Towards the end of your loan, the principle takes up the majority of the payment, with very little interest making up a part of the payment.

See the graph below showing the first 12 months of a $450,000 loan.

See how the first repayment is made up mostly of interest?

Now let’s take a look at the final payments of a 30-year loan. In this graph, most of the payment is made up of principle, with a very small interest component. The majority of your loan is paid off in the final years. This is due to the fact that interest is calculated on your loan balance.

Generally, you would set your Owner Occupied Property (where you live), to Principle and Interest repayments. This is so you build up equity in your home from the start and it safeguards you against property prices taking a downturn. You can later use the equity in your home to purchase your next home or investment property. It is wise to put extra money into your home loan if you can from the start, as any extra repayments will go towards reducing the principle faster and building up that equity quicker.

Interest-only repayments

Interest-only repayments, quite simply, means that you only pay the interest and make no payments off the principle. Most lenders will limit the amount of time you are able to do this and usually only offer this option to Investment lending. The interest-only period is usually 5 years and when it finishes, your loan rolls onto principle and interest repayments.

As an investor, you have the option to reset your interest-only period for 5-10 years at a time when your interest only period comes to an end.

During the 5 year period of interest only, your loan will not reduce at all.

See the graph below: Notice how the Balance remains the same over the course of 1 year?

Disadvantages to IO loans

It is important to note that once your loan rolls back to principle and interest after the 5-year interest-only term is up, your repayments will be more than they would have been if you had not taken the 5 yr IO term. This is because you now only have 25 years to repay the loan instead of 30 years. Your principle repayment will need to increase to allow for the 5 years you were not putting a dent in the loan amount.

Investors may consider resetting your entire loan term back to 30 years as part of a refinance, to maximize your serviceability and allow you to continue with interest-only repayments for a longer period.

Also, it is important to be aware of the difference in interest rates. Interest-only rates are often higher than the Principle and Interest rates.

Advantages to IO loans

So why would anyone want IO repayments? Well, there are a couple of reasons, particularly aimed at investors.

Your overall monthly repayments are lower as you are not making the principle payment. Keeping your monthly repayments down increases your borrowing capacity for additional property purchases or other investments. While investors are in the accumulation phase of purchasing property, interest-only repayments allow them to borrow more money and purchase more property, than they would otherwise be able to if their repayments were Principle and interest.

- Your balance does not reduce. Although this sounds like a negative, it can in fact be positive to an investor. Investment debt is tax-deductible debt. The more investment debt you have, the more of a tax deduction it is. Keeping your investment debt high, keeps your tax deductions at a maximum.

- Setting your investment lending to Interest only, allows you to put more funds towards your owner-occupied property and pay that down first. Owner-occupied lending is not tax-deductible, therefore you want to get rid of that debt as soon as possible.

- Speaking to a mortgage broker can help you decide which is the best repayment type for your circumstances. There are so many variables to consider and making the wrong decision can hinder your chances of borrowing down the track.

If you would like more information, please book in a time to speak with a Mortgage specialist.

Which is better, offset or redraw?

Offset

Offset accounts are like everyday transaction accounts, giving you easy access to your money at any time. The offset account is a separate account that sits outside of your mortgage. Money that you have sitting in the offset account will be "offset" against the mortgage. For example, if you have a $300,000 loan with $10,000 sitting in the offset, you will only be paying interest on $290,000. Most offsets attract an annual fee of anywhere between $200-$400, payable on the anniversary of your loan.

Redraw

Redraw facilities let you access extra repayments that you have made on your home loan over and above the required payment from the bank. They are not separate accounts. You will see how much money you have in the redraw as your mortgage will be in credit.

Which is better?

Both can help reduce the amount of interest you pay on your home loan but there are a few slight differences. Offsets are the most easily accessible, acting in the same way as a normal transaction or savings account. You can move money in and out by utilising your banking app, the same as your other accounts. Redraw can have a few more restrictions. Your lender may have minimum redraw amounts, delays in the funds being moved ie not instantaneous, or having to phone the bank or fill in a form to access the funds. If you have an investment property, there are also tax implications to consider so please talk to your accountant. Speaking to a mortgage broker can help you decide which is the best repayment type for your circumstances. There are so many variables to consider and making the wrong decision can hinder your chances of borrowing down the track.

Why does the lender need my Bank Statements?

Bank statements – What is the lender looking for?

In this article, we will talk about spending, saving, loan conduct and what the bank is looking for when they are assessing your loan application.

Spending

All banks use similar methods to assess how much a household is spending each month. Basically, there are 2 considerations:

- What you are actually spending.

- What similar families, in similar income ranges are spending (HEMS)

Lenders will look at these 2 figures and go off whichever is higher. Let's look at each more closely.

1. What you are actually spending

Most brokers use 1 of 2 apps for collating bank statements to see how much you are spending and what you are spending your money on.

- Bankstatements.com.au

- Cashdeck.com.au

Both of these apps require you to log into your account and bank statements will be sent to your broker showing spending over a 6-month period. The statements come with a breakdown of the categories of spending which is used to cross-check the expenses you have declared.

The main categories of spending are as follows

- Rent

- Utilities

- Groceries

- Dining Out

- Insurance

- Telecommunications

- Subscription TV

- Education and Childcare

- Vehicles and Transport

- Personal Care

- Health

- Department Stores

- Retail

- Home Improvement

- Entertainment

- Gyms and other memberships

- Travel

- Pet Care

- Uncategorised Debits

There are additional sections included in the bank statements summary such as Wages, Centrelink, Liabilities and Responsible lending flags to highlight gambling (including lotto), overdrawn accounts and dishonours.

Your mortgage broker will have a conversation with you about any discrepancies between your bank statements and your declared spending. If you have made one-off purchases like appliances or furniture, these can be removed to reflect average monthly spending more accurately.

2. What similar families, in similar income ranges are spending

The second method Lenders look at is what we call the HEMS (Household Expenditure Measure). HEMS is based off the results in the Australian Bureau of Statistics Household Expenditure Survey and compares families with the same number of adults and children on similar income levels.

HEMS is broken down into the following categories:

- Absolute basics - like food, clothes, utilities, communication and transport costs

- Discretionary basics - like entertainment, tobacco, alcohol, and eating out.

- Non-basics - more luxury items like overseas travel or home services like cleaners and gardeners

There are additional items that fall outside of HEMS and need to be added on top of the HEMS household spending. These include Child Maintenance, Strata fees, Private School Fees, Private Health Insurance & Personal insurance held outside of superannuation such as Life/TPD or income protection.

The lender will use the higher of the 2 figures. If your actual spending is below HEMS, the HEMS figure will be applied. If your actual spending is higher than the HEMS, then they will use your actual spending to assess your application.

There are some instances where this figure can be argued such as a fly-in/fly-out applicant who may be on a high income but is only home 50% of the time and has all food and expenses paid for while at work.

Using a combination of both methods, your broker will be able to get an accurate snapshot of your spending habits per month and this is used to assist in working out how much you can borrow.

Savings

Savings are much less complicated. Lenders just want to see genuine savings held in your bank account over a 3-month period. You may have savings progressively increasing as you credit funds to your account, or you might have received a lump sum by way of gift or inheritance with the balance remaining the same over the 3 months. It really does not matter. You can even withdraw from your savings account from time to time so long as at the end of the 3 months, you have the required amount showing as your balance.

There is a bit of confusion around using your rent payments as proof of genuine savings. Some people think if they are paying rent, then they don’t need a deposit but this is not the case. You still need to physically hold the deposit in your bank account. The rent you have paid does not replace the need for a deposit.

An example where we can use this policy is if you received a lump sum payment like a tax refund or inheritance that is not viewed as genuine saving as you have not held it in your account for 3 months. If your rent over the last 6 months is equivalent to that amount, the lender will view your lump sum as being genuine savings by considering your rental payments as well.

Another policy some lenders will consider is where a borrower has made accelerated payments on a loan to pay it out early such as a personal loan. These extra payments can also be used to argue genuine savings where a lump sum payment is being used.

Loan Conduct

When you apply for a loan, the lender will ask to see bank statements for any loans that you have. Checking your statements enables us to see if you are making your repayments on time and allows them to assess the level of risk in lending to each individual. Generally, we will collect 3-6 months' statements for any other home loans, credit cards or other personal debts.

Keeping your loans in order is important when preparing to apply for a mortgage. If there are missed payments or overdue amounts the lender may decline your application as they view you as a higher risk. This is imperative where mortgage insurance is applicable. Even 1 payment made over 1 month late, will impact your credit file and remain on your history for 2 years.

Undisclosed Liabilities

Bank statements will show the lender any payments for loans the client may have. These include credit cards, Afterpay, Zippay, Paypal pay in 4 and any other buy now pay later facility. We can also pick up on private debt arrangements with family where transfers are being made to one particular person. It is our job as your broker to go through your statements and ensure that all liabilities have been disclosed to the lender.

As your mortgage broker will also check your credit file before submitting your application to the bank to ensure it is clear.

What is debt consolidation and why would you do it?

1. Lower Interest Rates

Home loans generally have lower interest rates compared to credit cards and personal loans, which can reduce the overall interest you pay on your debts.

2. Simplified Payments

Consolidating multiple debts into a single home loan payment can make managing and keeping track of your financial obligations easier.

3. Improved Cash Flow

Extending the repayment period through your home loan may lower monthly payments, improve your cash flow, and make it easier to handle your finances.

4. Improved Credit Score

Closing debts can improve your credit score by reducing your credit utilization ratio and showing a consistent payment history.

5. Avoiding Penalties

Consolidating debts into a home loan can help avoid late fees and penalties associated with other debts if you struggle to keep up with multiple payments.

Consolidation using a Personal Loan

You don't need a home loan to do a consolidation. Let's look at Consolidating two Credit Cards into a Personal loan.

Credit cards certainly come in handy, however, if you are finding it difficult to pay them off, you might want to consider a debt consolidation with a personal loan.

Check out this hypothetical debt consolidation scenario……

This Client has 2 credit cards both at 26% interest.

On one card he owes $10,000 on the other card, he owes $7,000

His Total Monthly repayments for both Credit Cards are $501 per month.

In reality, there is a strong possibility that additional purchases would be made along the way, pushing up his monthly repayments and extending the time it takes to pay these cards off.

If he takes out a personal loan with us for $17,000. He could pay out both of his credit cards over a 5-year term. Depending on his particular circumstances and the rate applied, his repayments could be reduced drastically.

For example, if our clients had clear credit and were given a rate of 8.5% and no monthly fees, his new repayments would be $348 per month. This is $153 per month in savings.

If our client then puts this $153 per month he is now saving towards his loan repayments, he will pay off all his debt 1 yr and 9 months quicker.

Not only that, but you can’t keep pulling money out of a personal loan the way you can on a credit card. You are forced to pay it off in the allotted time no matter what. It takes away the temptation and ensures your debts are paid down, not to mention the extra cash in your pocket every month!

Another bonus is that your credit score will improve. Credit card debt is considered negative, whereas personal loan debt is considered positive. If you close your credit cards, you are essentially closing off the negative components on the credit score and your score should increase.

Why would you use a Mortgage Broker?

Best Interest Duty

The best interests duty (BID) for mortgage brokers is a statutory obligation for mortgage brokers to act in the best interests of consumers, and to prioritise consumers' interest when providing credit assistance. Every recommendation, every discussion and every option that is presented must be recorded with detailed reasoning attached. Consumers' files will be intermittently audited to ensure that Mortgage Brokers are following the new legislation precisely. We MUST act in the consumer's best interest if we want to continue to operate and avoid heavy penalties. Banks do not fall under this legislation. This means that if you go directly to a bank, they can act in their own interests ie present expensive options that might not be suitable, and not act in the best interest of the borrower. The legislation applies only to Mortgage Brokers, not banks.

More Options

If you go directly to the bank, you will be presented with a couple of loan products that they have on offer. The loan writers have targets they are expected to meet and they will present options that will benefit the bank the most. Expensive products, with loads of features that attract high fees, may not be in your best interest, however, as discussed above, the BID laws do not apply. If you go to a Broker, you will have thousands of different products to choose from. A Broker will sit down with you and go over all of your goals and needs in detail during the consultation, to ascertain exactly what it is you are trying to achieve. The Broker will then go away and do in-depth research based on this information. When products are finally presented to you, they will be in line with everything that you stated was important to you. The final product you choose will be the one that is the best fit for you.

Information and Education

When you see a Mortgage Broker, you will be given all relevant information that may apply to your circumstance, including the various Government schemes, Grants, and incentives. You will also be informed of any promotions offered by the various lenders such as cash-back offers, interest rate promotions, mortgage insurance discounts or specialist professional packages. You will be given as much information as you need in regards to features, repayment types and the different types of home loans to assist you in making an informed decision. A major part of a Mortgage Brokers role is to ensure the client is educated and well equipped to select a product that will best suit their needs.

Credit Scoring

This is a big one that most people don't consider. When you shop around from bank to bank, often the bank will do an upfront credit check at the start of the conversation to see if the client is a low enough risk to fit within their policies. Consumers will often not even realise that a check has been done until much later. When a bank runs a credit check, it will mark your credit file as an enquiry, regardless of whether you took up the finance or not. If you go from bank to bank and each of those lenders runs a credit check, you are very quickly running a tally of enquiries. These enquiries will in turn affect your credit score. Around 8 enquiries is ok but any more start to have a negative impact on your score, hindering your chance of securing finance in the future. Shopping around for finance is a huge mistake people make as they don't realise that every credit provider will mark their file. This includes all financial institutions - credit cards, zippay, zip money, car finance, personal loans etc etc.. You can see how easy it would be to acquire 8 or more in 5 years. If you see a Mortgage Broker, they can run a check on your file without marking your report with an enquiry. This is because they are not a lender. The Broker will be able to shop around on your behalf without a single enquiry being added to your file. This also applies to car finance and personal loans.

Bank Policies

With so many credit policies and guidelines, it is almost impossible for a consumer to know which bank is going to be right for their particular circumstance. You may walk into a branch that you have banked with your whole life, expecting to get approval, only to find out that you don't fit within their policies for whatever reason. Mortgage Brokers will be able to tell you who will lend to someone who is still on probation, who is great with construction, who will take family allowance or child support as income, who will accept a large rural block or a tricky postcode, and who has the most generous borrowing calculators. There are thousands of reasons to choose one bank over another and the policies are changing daily. Brokers get notified of every policy change and can quickly steer you in the right direction so that you won't get a decline for not knowing one of their rules or restrictions.

Post Settlement Service

Once your loan settles with your bank, their job pretty much ends there. Mortgage Brokers, however, have a lot to do post-settlement. You will be able to receive updates on new products, rate discounts, government initiatives or even market updates. Most brokers also offer their clients Annual Reviews, where they will check in with you to make sure you are still happy with your loan, update any additional goals you may have and ensure your current loan is in line with your goals, run valuations and pricing discounts on your behalf and just ensure that you are happy and satisfied. These reviews should be done every year around the anniversary of your settlement. We will also keep an eye on your fixed rate expiry dates and get in contact with you prior to see what you would like to do at the end of the fixed term. We can submit variations or top-ups on your behalf and basically be your personal contact for anything you need post-settlement.

What happens if I can't make my repayments?

Financial Hardship

All lenders must have financial hardship policies in place and all borrowers are entitled to this if they face unemployment and the like.

Remember if you contact your lender, straight up, you can stop or reduce your repayments under hardship circumstances. This means you do not get a mark on your credit report and you won't get a default. So long as you stick to the agreed arrangement that you make with your bank.

This applies to all finances, not just mortgages. You have to act fast and be upfront. Do not leave it until it's too late. If you do find yourself out of work, contact your lender immediately. If you let your payments fall behind then you are at risk of a decreased credit score and possibly a default. Once that is done it can't be undone.

Hardship is a short-term thing until you get back on your feet. You will have to submit your current household expenses and show that your current income cannot meet your expenses. Some lenders only allow you to go on hardship for 3 months whereas others have unlimited time.

Some lenders let you track what you owe back onto the loan and others literally hit the pause button until you are back on your feet. It's different for every bank and you have to keep the lines of communication open.

If you go to your lender website and type in financial assist or financial hardship, you should be able to find the terms and conditions applicable to you.

If you need help get in touch with us.

Financial Calculators

Need help planning a budget or want to know how much you can borrow?